Competitive Advantages: Fixed Rate vs. Variable Rate Lenders

Is a lower coupon rate necessarily a better choice—all things considered?

Bridging the Gap

Commercial real estate investors often seek a bridge loan if they are unable to obtain a conventional loan from a bank. These short-term solutions provided by alternative lenders are used for a variety of reasons—property rehabilitation and improvement, construction completion, or using the cash toward the purchase of another property are situations which require liquidity—often in short order.

Commercial financial institutions, with their stringent rules, creditworthiness tests, and cash flow and income thresholds are exclusionary to investors, if they don’t fit within the bank’s prescribed box. The outcome can be quite different in the alternative lending space where data, analytics and an asset’s collateral determine a business's credit risk.

Commercial real estate investors are often faced with a choice between a mortgage lender offering a variable vs. fixed rate. It leaves many wondering which makes the best sense over the term of the loan. Given the market volatility, we will take a look at the competitive advantages of both, and share expert insights to help decide the best path forward.

Commercial mortgage bridge lenders, such as Avatar Financial Group LLC (Avatar), work with a variety of businesses, investors and commercial property sectors to ensure that their lending needs are met successfully. Avatar’s commercial mortgage REIT provides hard money and bridge loans to businesses that need to meet their obligations with expedience. This REIT offers sponsors a competitive fixed rate at a more conservative loan-to-value ratio. Bridge loans can range from a few months to a few years, most landing between 12 and 24 months.

The nonqualified mortgage sector (non-QM) exceeded $3.8 trillion in 2020 and 2021 with industry analysts expecting market share to double in 2022, according to research by the Mortgage Bankers Association. Many banks increasingly are unable to commit to loans, as the combination of increasing interest rates, inflation and uncertainties about future property values make lending thresholds more difficult to attain.

During the historic low interest rate environment when money was cheap, qualified borrowers took advantage. Many opted for variable rates to finance their investments, hedging against prime without feeling an urgent need to purchase a rate cap to lock in a rate ceiling. In a declining interest rate market, a variable rate loan benefits borrowers because their loan payments will also decrease. In that environment it made perfect sense to roll the dice on a floating rate where little upward pressure could be seen. In today’s environment, investors are trying to assess whether it is best to opt for a variable rate over fixed, and what factors should be considered when comparing each option? To answer that question, it is necessary to assess the horizon.

Where Are We Now?

It is apparent to any commercial real estate investor that Q2 2022, looks dramatically different from Q2 2021. Inflation has skyrocketed year-over-year, driving interest rates up and the cost of borrowing, despite initial prognostications to the contrary. Banks find that they cannot get to the leverage many clients need to originate their loans. The last time the mortgage interest rate was at 5%, according to Freddie Mac’s historical weekly data, was May 6, 2010—a dozen years ago. So what options are available for investors who are unable to secure debt and need it fast? Avatar Financial Group LLC’s President, T.R. Hazelrigg advises that banks can be a good option, but access and speed-to-loan may be an issue. “Banks, for the right property and investor, can give you a great rate, but they also take a lot of time. It can be several months for a bank loan to close,” he explains. Bridge loans have higher rates than banks, but the loan closing window is condensed, typically in a matter of weeks. Depending on the type of property, and what third party reports are available, it could be as little as a week and in the case of Avatar, the loan rate is locked in,” he adds. When you are doing deals, time is money and meeting the close of escrow may be the difference between winning and losing out on an acquisition.

Why Cap Rates Matter

Real estate investors make investment decisions based on the projected cap rate of an asset. The capitalization rate provides a correlation between a property’s net operating income and value. Compressed, or lower cap rates occur when market conditions are strong and the economy is percolating, leading to higher real estate values. When these variables are assessed against a backdrop of rising interest rates, two considerations emerge. First, an investor must demonstrate a stronger income level, and second, produce a larger down payment—in order to qualify for that conventional loan. Consequently, the same financial tool the Federal Reserve is using to take some air out of the overheated economy, is narrowing the pool of bank loans being made to investors. Rising interest rates and uncertainty about property appreciation will sustain a strong demand for nonqualified mortgage lending, according to industry experts.

Avatar Tells A Story Loan

Avatar Financial Group LLC is in the business of commercial mortgage lending, and for the last two decades has experienced, and successfully managed its investment returns in fluctuating market cycles. The firm is a leader in commercial hard money bridge loans, offering solutions to investors who need to close deals quickly, or may not qualify for a conventional bank loan. The company was founded in 2003, and has returned 9.46% over the most recent 10-year period. In 2021, its Mortgage REIT produced an 8.64% weighted average return. Hazelrigg explains how Avatar’s success is anchored on a strategy of evaluating a potential lender against a different set of criteria than traditional lenders do. “Banks have a “Know Your Customer” standard that looks at the three C’s of lending: cash flow, character, and collateral. We are flipped in a sense; in that we don’t evaluate lending in that order. Our investment team looks primarily at the amount of collateral value in a certain property. We understand that there may be extenuating circumstances that can impact someone negatively. For example, that investor may have come out of a bad divorce, and their personal credit rating is not good. Or there may be a tax lien on the property that has little to do with its underlying value. We look at the amount of collateral and then consider the backstory. You can say that we make “story loans” and are flexible and economics oriented.” Post-pandemic, understanding an investor’s story can help uncover opportunities which has provided a tailwind to the alternative lending industry.

“SMILE” Pretty

Avatar Financial Group LLC makes investments nationwide with the most activity in the “Smile States” to help investors earn better returns. In real estate investment parlance this “smile” spans the United States, generally from coast-to-coast, dipping through the sunbelt states. This geographical diversification reduces risk and includes some of the economically fastest growing regions in the nation. Avatar lends in various asset classes within commercial real estate, including industrial, office, hospitality, multifamily and retail. Lending diversification across sectors, along with taking a senior debt position is an investment strategy that is designed to mitigate risk.

Variable or Fixed: What Should Investors Consider?

In this “new shifting normal” what should investors consider when choosing between a variable or fixed mortgage loan rate? Avatar suggests a competitive advantage can be gained via savvy strategies. “We are short term lenders,” Hazelrigg explains. “We don’t have to project too far into the future—just a couple of years. We feel that with only a two-year window, things are not going to change that much.” Hazelrigg points out that his company will hedge when considering the advance rate of a particular loan to build a cushion and manage risk. An advance rate is the percentage amount of the value of the collateral that a lender is willing to extend as a loan also known as loan-to-value (LTV). Avatar lends at a conservative loan-to-value ratio, usually between 60-70% of the appraised value of the property. This enables them to provide a better fixed rate to investors. Lending at a lower LTV ratio is generally deemed to be lower risk.

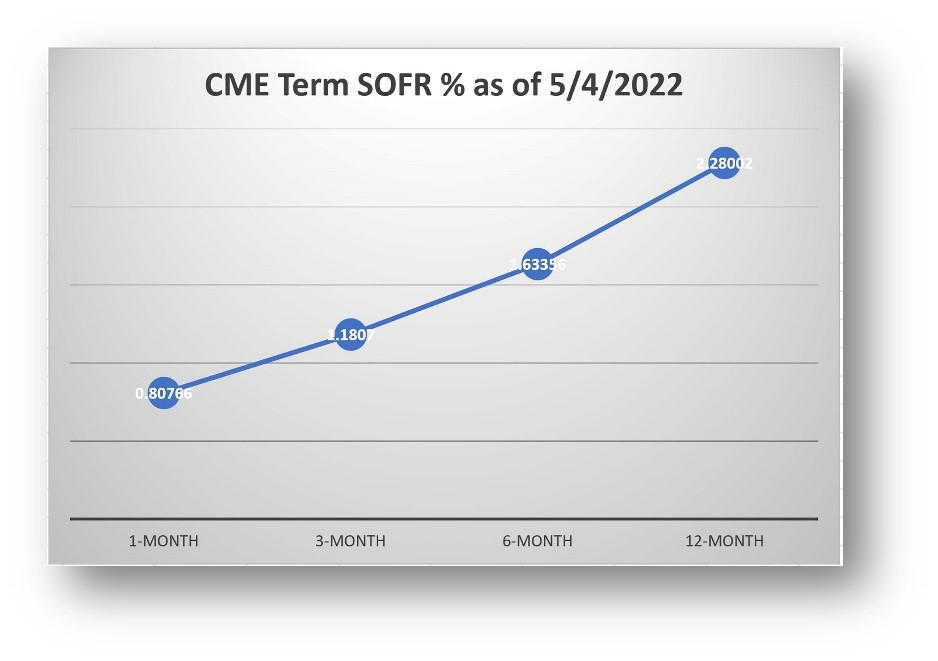

Secured Overnight Financing Rate, better known by the acronym SOFR, is an economic reference rate established as an alternative to LIBOR that will be fully transitioned by June 30, 2023, when LIBOR contracts will cease to be published. SOFR is an overnight rate closely correlating with other money market rates, including mortgage lending rates, and short-term borrowing costs. Rapidly becoming a key financial benchmark, the 1-month SOFR rate reported on May 4, 2022, was 0.81. According to CME Term SOFR Reference Rates, benchmark projections predict that SOFR may rise north of 2.2 by year-end, causing a sharp increase in the cost of a variable rate loan over time. Hazelrigg cautions that it might be a wiser decision to lock in a favorable fixed rate throughout the loan term given this expectation.

CME Term SOFR as of May 4, 2022

*Informational Purposes Only Data Courtesy of CME Group

Unlike many bridge lenders trying to make money on the spread between borrowed bank debt and the bridge lending rate, Avatar’s REIT is not a leveraged fund. Hazelrigg explains, “A lot of our competitors are in the business of trying to make money by borrowing at 3.5% and lending at 5%, for example. These competitors are at a disadvantage as the cost of their borrowed money is going up, while our capital structure is less affected. If you are borrowing money to lend it out, you cannot take a risk to lend for an extended period at an attractive fixed rate.” Avatar’s capital structure enables it to extend a fixed rate to customers for a two-year period. “We would rather have a fixed rate and not be trying to negotiate rate cap fees,” Hazelrigg explains.

Hazelrigg concludes with this analysis. “As an investor you should consider that although you may be able to acquire a loan at a lower rate, you are now faced with having to purchase a rate cap to prevent the rate from rising, let’s say, more than 2% over the course of a loan. Once you calculate the additional fees, not to mention the time and effort needed to secure it, that lower coupon rate may no longer look like such a good deal.” This evaluation is what every commercial real estate investor will need to carefully consider and weigh as investors and lenders navigate this volatile and uncertain environment together.